Now, what if we were to increase the frequency from yearly to monthly?

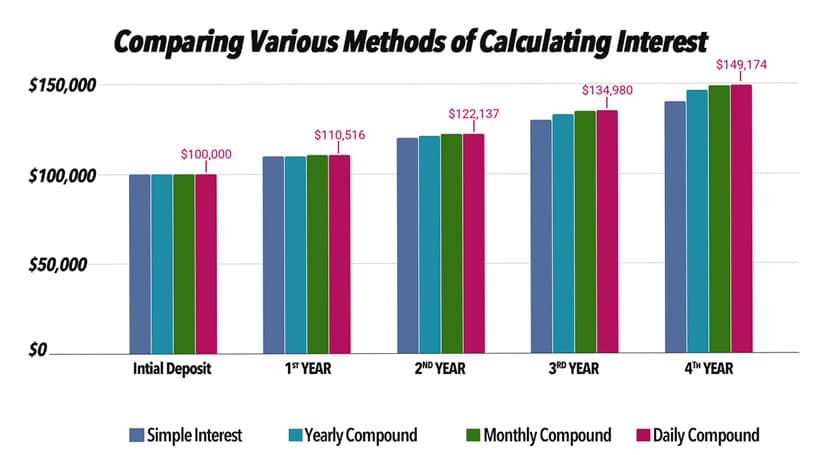

Looking at the chart below, we can see the comparison of all three, from simple interest to compound interest to monthly compound interest.

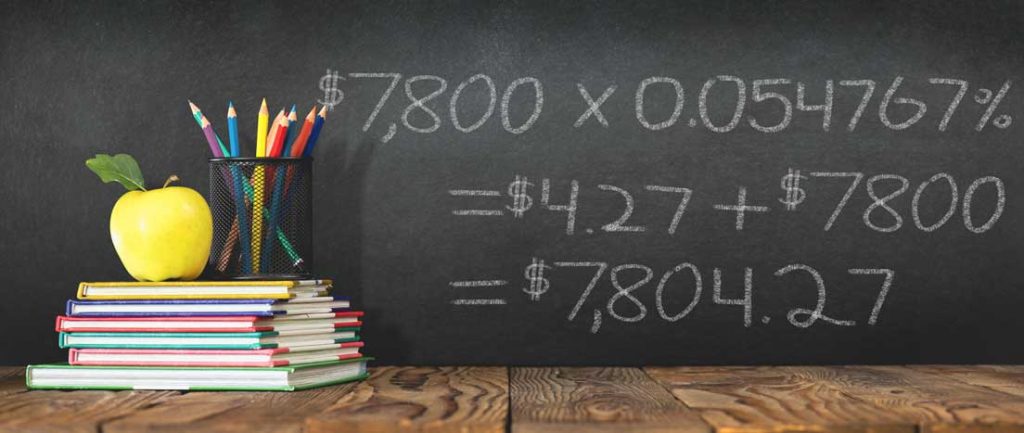

Simply put, instead of tallying up your interest annually, it’s performed monthly. That is to say, that your interest is added to your account at the end of every month. So using the same numbers from the previous example, our first month’s earnings would be $833.33, which is 1/12th of the total year’s interest.

After stacking the interest on top of your initial balance, you can see that your new balance at the end of the month corresponds to $100,833.33. Moving forward through each month – from February to March and so on – it’s easy to discern how successive growth is of an exponential nature.

This makes for some sweet returns using functional mathematics.

As you can see the difference that your financial institution pays you, over the course of one fiscal year, for maintaining an account that compounds monthly vs. yearly is $471.31.

That’s roughly 10 nights at the movies using your Scotiabank Scene Visa complete with 2 cold bevvies of your choice on the rocks and a large buttered popcorn. Not that buttery flavoured garbage – the real stuff!

So at this point, you’re asking yourself can we get a little deeper with this?

Why yes, of course, you can. Which brings us to our next and final frequency rate of compounding.